Exclusive

Big four ex-partner claims colleagues helped in tax exploitation scheme

A former big four accounting partner being sued for allegedly promoting tax exploitation schemes will claim others at his firm were involved in the drafting and review of documents.

The ex-partner also wants to file a limited defence to the Tax Office’s claims because he may incriminate himself and open himself up to penalties, according to an application made to the Federal Court by his legal team.

Last week, The Australian Financial Reviewrevealed that the commissioner of Taxation was suing the ex-partner in the Federal Court, alleging that he promoted three so-called Tax Loss Access Schemes to seven clients between November 2016 and April 2021.

The partner has applied for his name and the names of his former firm and clients to be suppressed, on the basis that he would be embarrassed and distressed if he were identified. Although that application was rejected in the first instance following opposition from the Financial Review and the commissioner, the partner is now seeking leave to appeal.

Following last week’s story, Greens senator Barbara Pocock sent a list of 17 questions to each of the big four firms. Two replied within a day that it was not their firm. However, the suppression order prevents the Financial Review from naming the firms that have denied that they employed the partner. The firm involved cannot reply because it would be in breach of the suppression orders by identifying itself.

The commissioner is seeking declarations of breaches and substantial fines. The maximum fine for an individual found to promote a tax exploitation scheme is the greater of $1.5 million, or twice the benefits obtained, for each year.

In a redacted draft defence, the partner’s lawyers said they might rely on the “involvement of persons at [redacted] including drafting or review of documents”.

The defence also stated that if the Tax Office was successful in proving part or all of the statement of claim, the ATO’s allegations did not meet the statutory definitions of a range of the allegations, such as tax evasion, tax exploitation scheme, promoter, and more.

The partner has also applied to file a limited defence because of self-incrimination and self-exposure to penalty. Federal Court rules require a respondent to file a defence.

The partner’s lawyers, however, asked the court to allow a limited defence because “compliance may interfere with his privilege against incrimination and exposure to penalties”.

Claiming privilege

In a redacted draft defence filed to the court, the former partner largely denies the allegations on grounds of privilege. Privilege against self-exposure to penalty is a legal claim which, at times, allows individuals to refuse to answer questions that could incriminate them.

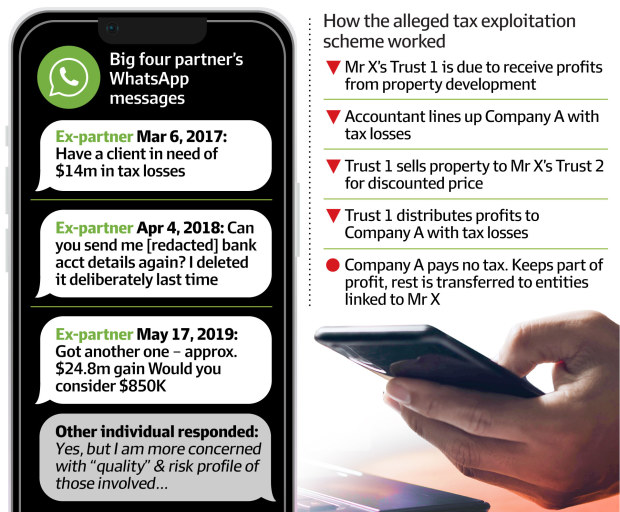

The alleged tax exploitation schemes involved the setting up of two trusts. When the client’s first trust was due to receive profits, for example from a property development, the accountant would line up a separate person’s company, which had past tax losses.

The first trust would sell the property to the client’s second trust for a discounted price, in one example at cost plus $1 million. The first trust would distribute profits to Company A, for example, which had the tax losses. Company A would pay no tax, keep part of the profit and transfer the rest of the money to entities related to the client.

The Tax Office’s statement of claim alleged that the former partner used WhatsApp to contact another individual when lining up the entity with losses.

The partner’s defence will also rely on the timing of the Tax Office’s case. The defence invokes the Tax Administration Act, which states that the commissioner cannot sue an entity for involvement in a tax exploitation scheme more than four years after the entity last engaged in conduct that would have been a promoter. However, the legislation also notes that the timing limitation does not apply to a tax evasion scheme.