Exclusive

Big four partner alleged to have promoted tax exploitation scheme

A former big four accounting firm partner is alleged to have helped clients reduce their tax on tens of millions in profits by shifting income to loss-making third parties who took payments for their part in the scheme.

The Commissioner of Taxation is suing the ex-partner in the Federal Court and seeking declarations of the breaches and substantial fines. The maximum fine for an individual found to promote a tax exploitation scheme is the greater of $1.5 million, or twice the benefits obtained, for each year.

The Commissioner alleged the former partner promoted three so-called Tax Loss Access Schemes to seven clients between November 2016 and April 2021. In separate litigation in the Supreme Court, two of the man’s clients are suing him over his tax advice.

The partner has applied for his name and the names of the firm and his clients to be suppressed, on the basis that he would be embarrassed and distressed if he were identified. Although that application was rejected in the first instance, following opposition from The Australian Financial Review and the Commissioner, it is under appeal.

The Tax Office and Treasury have signalled changes to tax promoter penalties laws in the wake of the PwC tax leaks scandal. This new case is one of only a handful of tax promoter cases brought to court under laws enacted in 2006.

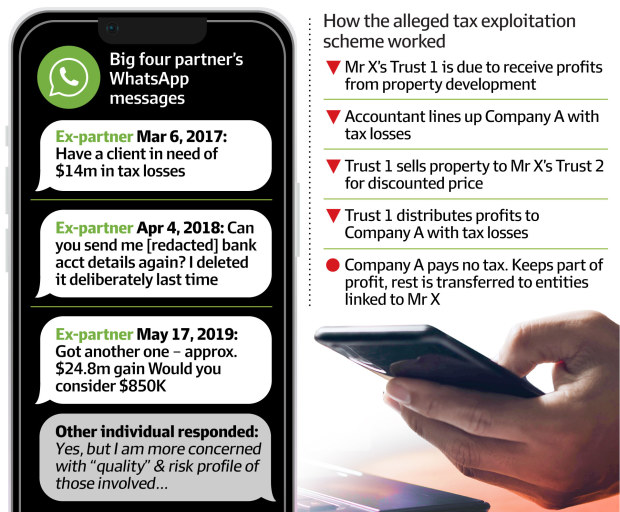

The scheme involved the setting up of two trusts. When the client’s first trust was due to receive profits, for example from a property development, the accountant would line up a separate person’s company, which had past tax losses.

The first trust would sell property to the client’s second trust for a discounted price, in one example at cost plus $1 million. The first trust would distribute profits to a Company A, for example, which had the tax losses. Company A would pay no tax, keep part of the profit and transfer the rest of the money to entities related to the client.

One scheme involved the construction of 55 units, which began in 2015. Towards the end of 2016 and into 2017, the former partner is alleged to have met with clients about the development. Profits were estimated to be around $10 million and the client “wanted to minimise the tax that would be payable on the profits from the sale of the units”, the ATO alleged.

The partner allegedly used a whiteboard to illustrate how the trust arrangements could work. A photo was taken of the whiteboard. In another instance, the client allegedly hand drew the diagram.

The ATO alleged the scheme meant the client “was not liable to pay tax with respect to that income” and “less tax was payable by one or more” of the beneficiaries of trusts than if they had not implemented it.

WhatsApp messages between the ex-partner and another individual, who is applying to suppress their name, alleged an understanding that a separate entity’s “tax losses could be used to absorb income or gains of [the partner’s] clients for a fee”, the ATO alleged.

‘Need $14m in tax losses’

“Have a client in need of $14m in tax losses...Can I tell him 5cents” the partner is alleged to have sent on March 6, 2018. The other individual responded “Sure...”

The 5 cents appears to represent a cost of 5 per cent for using tax losses.

The next month, the partner sent another WhatsApp message stating “got a small some [sic] read[y] to go $128k for $3.2m (ie 4c) with another two from the same guy. Can you send me [redacted] bank acct details again? I deleted it deliberately last time”.

In May 2019, the partner messages again: “Got another one – approx 24.8m gain Would you consider $850k”. The individual responded: “yes, but I am more concerned with “quality” &risk profile of those involved.”

The partner allegedly told clients the ATO had scrutinised similar arrangements and “found no issues with it”. He also allegedly said it was based on a High Court decision from 1989, that he had run it by a number of partners who advised it was a common arrangement and if there was any issue with the ATO it would not be related to the individuals or their associated entities.

The ATO alleged this was false information and he did not have reasonable grounds to make the statement.

Name suppression

The Financial Review and the Commissioner of Taxation successfully opposed the partner’s application to suppress his name, his clients’ names and his former employer.

Justice Geoffrey Kennett refused the partner’s application in early October, but the ex-partner is seeking leave to appeal that decision. The appeal process is expected to take weeks or months if leave is granted. If the partner is not granted leave for appeal, or the appeal is unsuccessful, their name, the firm and clients’ names will be released.

The partner made a further application to change Justice Kennett’s orders last week to stop access by the Financial Review. This was denied and this masthead was granted redacted versions of the statement of claim until the appeal process is finished. The ex-partner has filed a defence, but has failed to provide the court with a redacted version.

The Financial Review initially applied for access to the statement of claim in August. However, the Federal Court’s changes to the access regime earlier this year now invites parties to make suppression applications before access is given. Legal representatives for the Financial Reviewhave had to appear in court five times to fight for access.