Treasury eyes tax on $60b in family trusts

Federal Treasury has ramped up scrutiny of family trusts, revealing that about 1.7 million people received income of almost $60 billion from the tax-friendly trust vehicles.

Trusts are often used by families, professionals, private businesses and farmers to protect assets and split investment income between beneficiaries, to take advantage of lower marginal tax rates.

Treasurer Jim Chalmers: Making tax system “better and fairer”. Alex Ellinghausen

About 11 per cent of taxpayers lodging a tax return reported trust income in 2020-21, Treasury said in its annual review of tax concessions released on Wednesday.

The number of beneficiaries grew by 200,000 from a year earlier when Treasury first called out the growing use of trusts in its Tax Expenditures and Insights Statement.

The income from trusts includes distributions from family and discretionary trusts and some unit trusts including managed funds.

Economist Chris Richardson said Labor’s changes to the stage three tax cuts announced last week made the use of trusts for tax planning more attractive, due to the reinstatement of the 37 per cent rate for incomes above $135,000 and the top 45 per cent rate kicking in at $190,000 instead of $200,000.

“The changes notably boost the incentive for higher income taxpayers to incorporate and/or adopt trust structures,” Mr Richardson said. “That’s because marginal rates went up for high incomes and down for low incomes – a target rich environment for tax advisers. Watch out for income splitting and ways to convert labour to capital income.”

Treasury’s review of forgone revenue from tax breaks also included almost $50 billion for superannuation contributions and earnings, $27 billion for rental deductions by landlords and $10.5 billion for payments received under the National Disability Insurance Scheme.

Labor at the 2019 election promised to crack down on income splitting to minimise tax via discretionary trusts.

It proposed taxing distributions from trusts at a minimum rate of 30 per cent to raise $4.1 billion over four years and $17.2 billion over a decade. Labor scrapped the policy after losing the election.

Separate Parliamentary Budget Office analysis shows a spike in “income bunching” by trust beneficiaries at incomes just below the thresholds where marginal rates rise to 19 per cent, 32.5 per cent, 37 per cent and 45 per cent.

“There is an incentive for the trustee to minimise the overall tax paid on trust income by allocating income first to beneficiaries paying lower marginal tax rates – when a beneficiary’s income reaches the next tax threshold, any additional trust income allocated to this beneficiary will be taxed at a higher rate,” the PBO noted in a 2021 analysis.

“Thus, many trust income allocations see people end up with a taxable income just below a tax threshold, consistent with minimising the overall tax paid on trust income.”

Treasury secretary Steven Kennedy in a public speech in June 2022 spoke of the “substantial opportunities for tax planning” in the tax system.

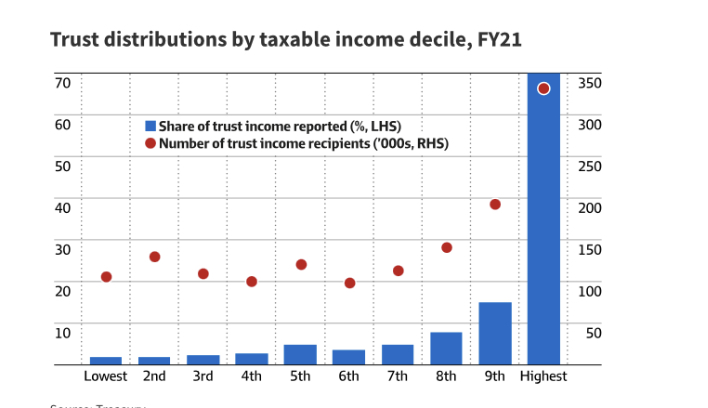

In new evidence that trusts were being used to stream income to lower income taxpayers such as family members, Treasury said 74 per cent of individuals reporting trust income had taxable incomes of less than $120,000.

Some 23 per cent of individuals who reported trust income were in the top 10 per cent of taxpayers, accounting for 61 per cent of all trust income reported.

“In 2020–21, 34 per cent of those who reported trust income had taxable incomes between $0 and $45,000, accounting for 9 per cent of all reported trust income; and 57 per cent had taxable incomes between $45,000 and $200,000, accounting for 52 per cent of all reported trust income,” Treasury noted.

“Of total trust income reported by individuals, 39 per cent is from individuals with taxable incomes above $200,000.”

Women and men evenly split

Slightly more women (830,000) reported trust income than men (820,000).

However, men reported a marginally larger share of reported trust income because they reported an average trust income of $37,410 in 2020–21, while women reported an average of $35,060.

Less than 0.5 per cent of trust beneficiaries were children aged under 18.

Usually, under 18s receiving trust distributions cannot take advantage of the $18,200 tax-free threshold. They are typically liable for higher tax rates on amounts above $416, except in limited circumstances such as money inherited via a testamentary trust when a parent dies.

Former Liberal treasurer Peter Costello tried to change the tax rules for trusts in 2002 in response to the Ralph review of business taxation but a revolt by the Nationals and some Liberal MPs forced him to back down.

Trusts are popular with farmers and small business owners for succession planning, asset protection, income splitting and tax minimisation.

Treasurer Jim Chalmers said in a statement that the Tax Expenditures and Insights Statement offered a detailed picture of how the tax system affected individuals, businesses and other entities, “as well as the pressures they place on the budget”.

“The Tax Expenditures and Insights Statement is a requirement under the Charter of Budget Honesty – it’s not a statement of policy intent,” Dr Chalmers said.

“We’re giving bigger tax cuts to more Australians to help with the cost of living, while making our tax system better and fairer.”

Expert coverage of Australia’s public sector.

Sign up to the Inside Government newsletter.

John Kehoe is Economics editor at Parliament House, Canberra. He writes on economics, politics and business. John was Washington correspondent covering Donald Trump’s election. He joined the Financial Review in 2008 from Treasury. Connect with John on Twitter. Email John at jkehoe@afr.com

Australia is too reliant on slugging workers for income tax – sapping work incentives, deterring international talent and penalising working-age people.

The political fight over the rejigged stage three income tax cuts is regrettably pitting workers against other wage earners.

This is not the tax reform debate Australia should be having. People are squabbling over a seemingly fixed $20 billion envelope to return bracket creep to personal income taxpayers.

This ignores all the warnings from Ken Henry’s tax review, the International Monetary Fund, the Organisation for Economic Co-operation and Development and economists surveyed by The Australian Financial Review on the performance of Treasurer Jim Chalmers.

Australia is too reliant on slugging workers for income tax – sapping work incentives, deterring international talent, penalising working-age people trying to get ahead in life and encouraging tax planning via self-employed incorporation, trusts and negative gearing.

Australia should be aiming for lower, flatter income taxes for workers and broadening other less economically damaging tax bases to pay for this.

Spending restraint, particularly on the out-of-control National Disability Insurance Scheme, is also paramount to afford tax reform.

Raising and/or broadening the 10 per cent goods and services tax, broadening land tax to the principal place of residence, stronger resource profit taxes, taxing the tax-free earnings of superannuation accounts with balances of up to $1.9 million in retirement and tightening up the use of trusts are all worthy ideas to pay for real income tax cuts.

Australia taxes “active” or “earned” income from wages and salaries too heavily and lightly taxes most forms of personal capital or “passive” income.

Regrettably, the latest changes are yet another Band-Aid and sticky tape approach that has bedevilled Australia for more than 20 years.

Values-based decision

This is a values-based decision by modern Labor, emboldened by cost-of-living pressures and a political objective to reconnect with middle Australia.

Initially, this will be paid for by higher earners on more than $146,486, largely due to the reinstatement of the 37 per cent rate at incomes above $135,000.

Over coming years, as inflation and nominal incomes rise, people currently earning $120,000 to $130,000 will be caught – largely explaining why Labor’s change generates $28 billion more tax over a decade unless governments in the future lift income tax thresholds.

The different impacts of Labor’s and the Coalition’s policies on average tax rates, work incentives and labour supply at different ends of the income spectrum are likely to be relatively modest.

All taxpayers will benefit from the bottom rate dropping from 19 per cent to 16 per cent, which Treasury estimates will add a tiny 0.25 per cent extra work hours to the labour market as part-timers are drawn in.

One would hope Treasury – which seconded tax-transfer expert Miranda Stewart – could provide much bolder reform options, such as America’s earned income tax credit (EITC) to cut high effective marginal rates for people moving from government support payments to work.

Treasury secretary Steven Kennedy warned last year that a secondary earner working more than one day a week on a full-time equivalent salary of $60,000 loses 60 per cent to 80 per cent of their income due to higher income tax, the withdrawal of family payments and childcare costs.

Instead, we got a rushed recalibration of stage three.

The Coalition’s stage three tax cuts attempted to lower and flatten tax rates, by eliminating the 37 per cent rate so that about 95 per cent of workers would pay no more than a marginal rate of 30 per cent for incomes up to $200,000.

While offering some appeal, the Coalitions’ policy still had problems. First, a failure was not using the $20 billion in annual income tax relief to “buy” broader tax reform. John Howard and Peter Costello introduced the GST in return for eliminating nuisance state taxes and cutting income tax.

The Coalition or Labor could have offered even larger stage three tax cuts across the income spectrum by broadening other more growth-friendly taxes.

High by international standards

Second, the top rate of 47 per cent (including the 2 per cent Medicare), is too high and kicked in at a relatively modest $200,000 (revised to $190,000).

This is more punishing than the United States, Canada, the United Kingdom and New Zealand, both in currency-adjusted terms and as a multiple of the minimum wage.

New Zealand has a flatter structure with no tax-free threshold and marginal rates ranging from 10.5 per cent to 39 per cent. The Kiwis have a 15 per cent GST, with far fewer exemptions. In contrast, Australia’s GST exempts private school fees, private health insurance and fresh food.

New Zealand enjoys a much higher labour force participation rate (percentage of population) of about 72 per cent, versus 64 per cent for Australia. Perhaps its lower and flatter tax scales are partly responsible, among other socioeconomic reasons.

Former Labor prime minister Paul Keating and former ACTU secretary Bill Kelty have backed a top marginal rate of 40 per cent. There are no aspirational Keatings or Keltys in the senior ranks of modern Labor, which is more focused on redistribution.

In Australia, a person earning $200,000 or $250,000 (pre-tax) in high-cost Sydney and Melbourne trying to pay a mortgage or rent and raise a family is often not wealthy these days.

Accountant Graeme Troy calculates that a mid-30s professional on an annual package of $260,000 (including superannuation) and a partner with three young children pays $76,075 income tax, $25,750 compulsory super, $80,000 family living costs and childcare, $46,800 rent in Sydney, $3000 in private health insurance, up to $23,424 for education loan repayment, $4000 income protection insurance, $16,000 motor vehicle expenses, $3000 for travel and tolls to work. They have no income splitting with their partner.

In contrast, a retired home-owning couple who are debt-free and have no dependents can receive $260,000 in tax-free pensions from their self-managed superannuation fund and can each utilise the tax-fee threshold to boost combined annual tax-free income to over $300,000, Troy says.

Trusts under scrutiny

Third, the top 47 per cent rate creates a big tax arbitrage for lawyers and accountants.

Treasury has dismissed the notion that Labor’s tweaks will make much difference to tax planning because there has already been a rapid growth in the use of discretionary trusts to split income. This seems defeatist.

Parliamentary Budget Office analysis shows a spike in “income bunching” by trust beneficiaries at incomes just below the thresholds where marginal rates rise to 19 per cent, 32.5 per cent, 37 per cent and 45 per cent.

Higher tax rates and lower income thresholds also make it more attractive for people to leverage into investment properties to negatively gear and reduce their income tax bills.

Moreover, why pay 47 per cent, when you can incorporate as a self-employed tradie or consultant and pay the small company tax rate of 25 per cent? (Incidentally, the 25 per cent small company rate is a silly distortion that should be increased back to 30 per cent until there is a uniform cut to the 30 per cent rate for all companies.)

The dirty little secret is that Liberals and Labor both like the 47 per cent rate for different reasons. Progressives like to tax the so-called “rich”. Liberals want workers to incorporate to make them small business voters and avoid being unionised employees.

The substance of the tax changes by Labor is somewhat symbolic. Labor is more redistributional than the Coalition. But the whole episode highlights how broken the tax system is and how both sides of politics are avoiding real tax reform.

The bigger worry is that Labor’s broken promise on tax erodes trust in politicians and makes it harder to convince voters of the need for proper tax reform to drive work incentives and reward hard work.